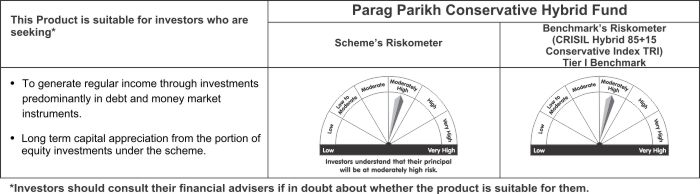

| Name of the fund | Parag Parikh Conservative Hybrid Fund |

| Investment Objective | To generate regular income through investments predominantly in debt and money market instruments. The Scheme also seeks to generate long term capital appreciation from the portion of equity investments under the scheme. However, there is no assurance or guarantee that the investment objective of the Scheme will be realized. |

| Type of the scheme | An open ended hybrid scheme investing predominantly in debt instruments. |

| Date of Allotment | 26th May 2021 |

| Name of the Fund Managers | Mr. Rajeev Thakkar - Equity Fund Manager (Since Inception)

Mr. Raunak Onkar - Equity Fund Manager (Since Inception) Mr. Raj Mehta - Debt Fund Manager (Since Inception) Mr. Rukun Tarachandani - Equity Fund Manager (Since May 16, 2022) |

| Month End Expense Ratio | Regular Plan: 0.62%* Direct Plan: 0.32%* *Including additional expenses and GST on management fees. Total Expense ratio is as on last business day of the month |

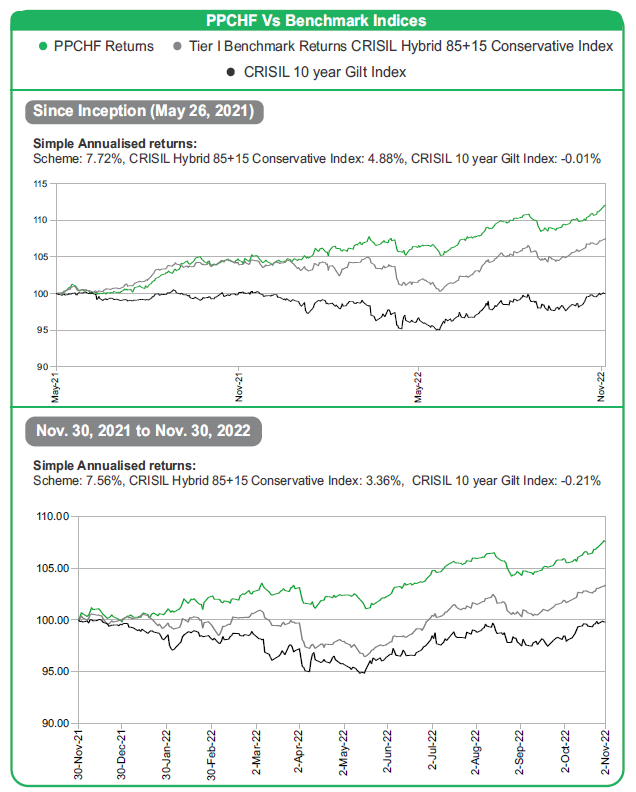

| Tier 1 Benchmark Index | CRISIL Hybrid 85+15 - Conservative Index TRI |

| Additional Benchmark | CRISIL 10 year GILT Index |

| Minimum Application / Additional Purchase Amount |

New Purchase: ₹ 5000 and in multiples of ₹ 1

thereafter. Additional Purchase: ₹ 1000 and in multiples of ₹ 1 thereafter. |

| Minimum SIP Investment Amount | Monthly SIP: ₹ 1,000, Quarterly SIP: ₹ 3,000 |

State Development Loans (SDLs) explained…

State Development Loans or SDLs as they are more commonly known, are issued by the State Governments to fund

their fiscal deficit. Each state can borrow up to a set limit. SDLs service their interest at half-yearly intervals and repay

the principal amount on the maturity date.

Rating agencies such as CRISIL & ICRA provides the prices of these SDLs every business day.

The RBI manages these SDL issues. RBI also makes sure that the SDLs are serviced by monitoring payment of

interest and principal. The RBI has the power to make repayments to SDLs out of the central government allocation

to states. The Reserve Bank of India maintains a fund that provides contingent liabilities arising with respect to

borrowings by undertakings of the state.

Mutual funds, pension funds, provident funds, commercial banks, insurance companies invest in these SDLs. Also,

individual investors can now invest in State Development Loans (SDLs) securities through the RBI platform. In 2015,

the Government permitted Foreign Portfolio Investors (FPIs) for buying SDLs of up to 2% of outstanding SDLs in the

market in a phased manner upto 2018.

SDLs are relatively illiquid compared to the Government securities (G-Secs) and that can be seen in the daily traded

volumes. Lack of liquidity can be attributed to low outstanding stock of multiple SDLs, market microstructure and lack

of market makers. It is also because insurance companies and provident funds hold a major proportion of the

outstanding issues and they are largely hold to maturity investors.

The commonly asked question relating to SDLs is with respect to the credit risk. SDLs are classified as sovereign and

the RBI has the power to repay the SDLs out of the allocation of taxes to be received by the State Governments.

The absence of the credit risk can be seen from the fact that risk weight assigned to holdings of SDLs by the

commercial banks in calculating the Capital to Risk (Weighted) Assets Ratio (CRARs) under the Basel III regulations

is zero - similar to that assigned for Government securities*.

* Source : RBI Bulletin dated 11th September 2018

Raj Mehta

December 8, 2022