This year's Budget made the NPS more attractive by making 40% of the corpus tax-free at retirement. This changed the tax status of NPS from 100% EET to 60% EET and 40% EEE.

What followed was increased demand from corporate employees, prompting more companies to offer the provisions of Section 80CCD (2) that allows companies to invest up to 10% of an employee's basic salary in the NPS on their behalf. The NPS' rising popularity is evident from the fact that 63.12% of corporate employees who joined NPS in July 2016 are from the 26-35 years age band, up from 46.38% just a month ago. Now though NPS offers several advantages, experts warn against rushing in to subscribe.

Use our checklist to figure if NPS really suits you. First consider your cash flow. The employer's contribution to NPS is deducted from your salary. In most cases, the salary structure is tweaked for the purpose. "If an employee opts for the maximum (10% of basic), the take home will come down to that extent. Are they ready for that?" asks Amol Joshi, Founder, PlanRupee Investment Services. Accept this offer only if it will not strain your finances.

Next, consider the liquidity of your investment. NPS is not for you if you want high liquidity throughout its tenure. NPS does not provide liquidity till 60. "The Section 80CCD (2) route is good for those who have disposable income and can lock-in that for the long term," says Manoj Nagpal, CEO, Outlook Asia Capital.

The third factor to consider is the current tax savings potential. As 60% of the NPS still works under the EET regime, treat it as tax deferment rather than tax saving. NPS is not useful for employees who have not exhausted their 80C limits of ₹ 1.5 lakh. Instead of NPS, they should concentrate on other options like PPF, ELSS, etc that are still under the EEE regime. "This structure suits employees with high salaries who want tax savings avenues beyond the ₹ 1.5 lakh restriction under 80C," says Nagpal. Now consider your asset allocation. NPS is a good option if you want to increase exposure to equity by a bit. However, it does not work for investors who are predominately invested in debt at present and want to route some additional investments to equities. The NPS does not allow equity exposure beyond 50%.

A new lifecycle fund introduced last week allows up to 75% equity exposure up to the age of 35 and then progressively brings it down by 2% every year. So, by the time one is 40, the exposure will not be more than 65% and will drop further to 55% by age 45. Does it mean that you can forgo the tax deferment option now? "Since historically equity has generated better returns in the long term, it makes sense to pay tax now and invest the remaining in equity mutual funds," says Joshi.

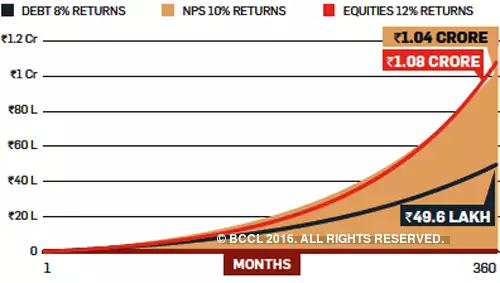

To test this theory, let's assume 12% return for equities, 8% for debt and 10% for NPS (when asset allocation is 50% equity and 50% debt). In the first option, an employee routes ₹ 5,000 a month to NPS (10% of a basic of ₹ 50,000). In the second and third options, the employee invests the remaining money after paying 30% taxes (₹ 3,500 a month) into equity or debt mutual funds. As the chart shows, the return on investments of ₹ 3,500 per month into equity funds overtakes the returns on ₹ 5,000 a month in NPS for 30 years, the returns from the equity investment will be more than that from the NPS.

Equity gives more from less

Assuming an employee invests ₹ 3,500 per month in a debt or equity fund instead of ₹ 5,000 a month in NPS for 30 years, the returns from the equity investment will be more than that from the NPS.

Due to the power of compounding, the final corpus of smaller investments growing at a faster rate will be higher than that of higher investments growing at slower rates.

The analysis does not consider the tax implication of NPS at maturity. If 30% tax on 60% of the accumulated corpus is considered, returns from equity would have overtaken that of NPS earlier. "Investors who want high equity exposure should wait till the equity component in NPS goes up to 75%," says Joshi. The current tax slab and expected tax slab on retirement are the fifth factors to consider. This is because you are only deferring tax. It makes little sense to defer 10% tax now and end up paying it at 20% or 30% on maturity.

On the other hand, it makes sense to defer tax now at 30% and pay it later at lower rates, say 10% or 20%. The employers' contribution under 80CCD (2) is more beneficial for employees in higher tax brackets. Since the 80CCD (2) restriction is linked to the basic pay and not to a fixed amount, the tax deferment potential is huge for highly paid employees. Now consider spending habits. Once you opt for the scheme, it acts like compulsory saving. "This will be in the form of monthly deduction from the salary and will be compulsory savings for those who are not saving enough now for retirement," says Nagpal. Finally, consider the compulsory annuity provision (NPS subscribers have to invest 40% of accumulated corpus into low yielding and taxable annuities). If the interest rate structure comes down in coming years, this low annuity rates may go down further.

The original article could be seen here.