The new Sebi guidelines on disclosures will bring transparency, but investors need to correctly interpret it

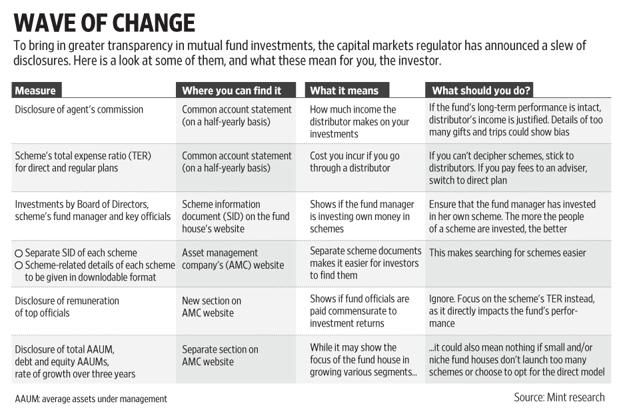

On 17 March, Sebi issued a circular that increased the level of transparency in MFs by a few notches. Among many changes, it has mandated fund houses to disclose the amount of commission that distributors earn on each scheme that the investor invests in, and it also directed mutual funds to disclose the salaries of top officials on their websites.

So, with all of this information made available to the MF investor, the question now is: how does one make sense out of it? Mint Money tells you what you should do.

Distributor commissions

Beginning October 2016, you will now come to know the commissions that your distributor earns. This information will be available as a part of the half-yearly common account statement, CAS, (a statement of your MF holdings across all the fund houses that you have invested in). The Sebi circular mentions that your distributor’s commission must be given in absolute terms (in rupees) and for each MF scheme that you may have invested in. So let us say you have invested in three schemes of the same fund house and all of them through the same distributor. Even in such a scenario, you will now get to know how much commission your distributor has earned (during the half-year period) on each of those schemes.

The commission paid will be the sum total of monetary payments as well as gifts, rewards and trips that your fund house may have organised for distributors, of which your own distributor may have benefited from or has been part of. Actually, this is not the first time that the capital market regulator has nudged distributors to disclose their commissions.

“Sebi had mandated the disclosure of commissions in a circular a few years ago (2009, when it had abolished entry loads). Distributors are supposed to tell their clients how much commission each fund pays. The current disclosures will not matter for certain customers who are aware of commissions or who are comfortable with the distributor they have. For others, the thought will go towards value addition by the distributor, and if that is missing, then alternate channels could be sought out,” said Rajesh Krishnamoorthy, managing director, iFast Financial India, the firm that runs Fundsupermart.com.

In its 2009 circular, Sebi had merely stated that distributors have to disclose commissions that they receive from schemes they aim to sell to the investor as well as commissions received from competing schemes. Last week, Sebi upped the ante and made the commission disclosure mandatory in the account statements of investors.

Understandably, the distributor community is not happy. Some say that disclosure of commissions could lead to passbacks. The practice of passback of commissions—whereby a distributor gives a part of her commissions earned from MFs to the investor—is banned, but is said be happening in a section of distributors. Some say that this might now increase. “For first-time investors in equity funds, seeing a negative return along with the positive commission expense may not go down well,” said the chief executive officer of a small-sized fund house who did not wish to be named. He adds that bank-based distributors may escape the intent of this disclosure, even if their commissions levels are unrealistic to the value of advice they give, and that smaller distributors will be the only ones who will “bear the brunt”.

Many bank customers have several relationships with the bank at any given point (such as savings bank account, credit cards, loans, using bank accounts to pay utility bills). Due to this, customers may hesitate in moving away from banks even if the new commission disclosures reveal startling figures.

On the other hand, financial advisers, especially those registered with Sebi, are happy with the increased transparency. “We started our business by disclosing commissions and letting the client know about various costs. So, most of our clients, whether on a fee-based service or otherwise, are aware of the commissions,” said Varun Girilal, co-founder and executive director, Mitraz Financial Services Pvt. Ltd. He also said that it is wrong to say that investing, even through online robo advisory channels, is free. “There is an embedded cost and clients should be made aware at the start to reduce conflict of interest,” he said.

Such disclosures not only increase transparency, it is beneficial for the investor. “However, especially for first-time investors, there may be a need to educate them about non-linear returns in asset classes like equity. It can take some time for the investment to show the desired result,” said Vishal Dhawan, founder and chief executive officer, Plan Ahead Wealth Advisors. He said that this information should be made available in the account statement so that the link can be established between the product, expenses and returns.

What should you do? The answer to this is not simple. Your distributor’s income is justified only when you make money in the long run. And making money doesn’t just mean selling you a good pedigreed scheme. It is also important that the scheme helps you meet your financial goal, which is, usually, years down the line. And to reach there, you will in most likelihood, face volatility in the interim. So, keep an eye on your fund’s performance vis-à-vis its benchmark. As long as it outperforms the benchmark consistently you are in good hands, and your distributor’s income is justified. However, if your fund keeps underperforming its benchmark, your distributor may have sold you a lemon. Her commission details, especially the gifts and foreign trips (how these non-monetary details will get disclosed in your CAS is still to be seen) might give you an idea of why she would have sold you that scheme.

What is the expense ratio of a direct plan?

Your CAS will also have information on the expense ratio of both the direct plan and regular plan of a scheme you have invested in. However, many feel this is futile. And they say this could actually hurt distributors and investors in falling markets. “In falling markets, the investor will see red in her portfolio, and she will also see the commission paid to the distributor. It would be natural for her to have thoughts like: When my money is eroding, why is my intermediary still being paid? The intermediary has to do a lot of work, especially in market down cycle because that is where the hand-holding helps. I fear that investors might not be able to see beyond short-term paper loss and might end up sacrificing long-term growth potential,” said Amol Joshi is founder, PlanRupee Investment Services.

Others question how this will benefit the industry and investors. “Is this disclosure going to increase penetration of mutual funds? How does it protect investors?” asked Roopa Venkatakrishnan, a Mumbai-based MF distributor.

What should you do? If you are a first-time MF investor or you don’t know which schemes to pick and how to choose them, or even if you know MFs well but don’t have the time to manage your portfolio, stick to an adviser or a distributor. If you go through a distributor (who earns commissions from fund houses and does not charge you fees), you will be invested in a regular plan. In that case, ignore the direct plan’s expense ratio. If you go through an adviser who charges you fees, make sure you are invested in the direct plan. Either way, you should keep an eye on your fund’s long-term performance. And do not let short-term market volatility judge how much your distributor is making.

Fund manager’s salary

It’s not just your distributor’s income that Sebi wants you to know. Effective 1 April 2016,your fund house will also now be required to disclose salaries of all its fund managers, its chief executive officer (CEO) and all senior employees whose salaries are in excess of Rs.60 lakh per annum. These disclosures will need to be made prominently on a fund house’s website.

Fund houses are already mandated to disclose the salaries of those employees who are deemed as ‘Key Officials’ (this includes CEO, chief investment officers, fund managers, chief operating officers and other such senior names who are crucial in heading various operations within a fund house and whose names come in a scheme’s statement of additional Information) in the asset management company’s annual report.

But now salaries of any one who earns more than Rs.60 lakh a year (not just key officials) will have be disclosed. Besides, the disclosures can no longer be hidden in a company’s annual reports. They will have to be displayed in a separate section on the fund house’s website.

Here too, a large section of the industry did not approve of the move. “The expense ratio that the scheme charges is regulated and capped by Sebi. Anything beyond that is anyway absorbed by the fund house and shareholders. An additional disclosure of the break up of total expense ratio may not add value to investors,” said Sundeep Sikka, chief executive officer, Reliance Capital Asset Management Ltd.

However, there is a segment of the industry that feels this is a good move.

“This is a step in the right direction. Salaries of senior officials are already listed in the annual reports. All Sebi has done is widened the ambit of such officials a bit,” said Akshay Gupta, chief executive officer, Indiabulls Asset Management Co. Ltd. Gupta also cautions that if such disclosures if made for only one financial instrument (in this case mutual funds) and not for others such as insurance, it can create a distortion.

Jimmy Patel, chief executive officer, Quantum Asset Management Co. Pvt. Ltd, made an interesting point. “Disclosing staff remuneration can be seen as an element of cost and in any case is required by company law, but has human resources issues. However, the focus needs to be on functions and cost rather than only on people. For example, it’s good if a fund house is spending on research and investment staff as that is the core business. This could be contrasted with the marketing function staff spends, to see where the focus of the asset manager lies,” he said.

What should you do? Don’t get obsessed with this detail. Ignore the salaries and instead focus on your scheme’s long-term performance. It is just a matter of transparency that fund manager salaries are disclosed in the public domain so that the fund manager know that in addition to making money for themselves, it’s also important to keep making money for investors.

Fund manager’s investments

If your fund manager asks you to invest in her fund, isn’t it good to know whether or not she has invested her own money in it as well? Sebi has not made it compulsory for fund managers to invest in their own funds yet, but it has asked fund houses to disclose how much each fund manager has invested in all the schemes that she manages.

Beginning 1 May 2016, all fund houses will have to disclose in every scheme’s information document, the aggregate investments made by its Board of Directors, fund managers and other senior employees, also known as key managerial personnel or key officials.

In February 2014, Sebi had said that all fund houses were required to put in 1% of their own money, called seed capital, subject to a maximum of Rs.50 lakh, in all their open-ended mutual fund schemes. Existing and new funds were asked to comply. In May 2013 when PPFAS Asset Management Pvt. Ltd launched its first (and till date its only MF scheme) equity fund, , it publicly disclosed that all its senior employees would invest in the scheme. As on the end of February 2016, 12.46% of the scheme’s corpus (Rs.596 crore) or close to Rs.75 crore belong to the employees of the firm.

“There is no guarantee that an investment will work out for unitholders. However, when the managers of the fund and key personnel invest in the scheme it aligns the interests. It helps in avoiding excesses like launching sectoral funds at peaks. It forces the attention of the fund house to the task of managing of investments rather than just asset gathering,” said Rajeev Thakkar, chief investment officer and director, PPFAS Asset Management Pvt. Ltd.

What should you do? It’s good to know how much your fund manager invests in a scheme. For instance, if your fund house launches too many schemes regularly or multiple schemes that are similar, it’s good to check if its senior officials have invested their own money in them.

The original article could be seen here.