Without fair pricing there isn’t another strong reason to choose an unlisted stock over a listed one

Domestic equity markets had been in focus in the past year with the benchmark indices seeing a 30% rally in 2014. This has lent optimism to the primary market as well. However so far this year, we have only seen a couple of initial public offerings (IPOs) closing, but there are more to come with at least three more issues in the pipeline that are ready to hit the market.

For retail investors, IPOs are projected almost like mystical beings, which appear at special times and make investing worthwhile. Returns for IPOs are always expected to be superlative with the ability to surpass returns from other listed shares.

However, the IPO experience in the recent past has not been encouraging. Share price of Ortel Communications Ltd, for instance, has been falling since it was listed on 19 March. Adlabs Entertainment Ltd had to reduce its IPO’s offer price and extend the closing date of the issue as demand was low.

Retail investors, however, continue to view IPOs as a secure door to enter the equity arena. This is why we saw high oversubscription in the retail investor quota for IPOs in 2014. But the reality is quite the opposite. Before you jump in to applying for IPO shares, here are some things you should understand better.

Pricing, pricing, pricing

It’s really all about the pricing. Pricing refers to the issue price at which you can buy shares of the company. There are many elements that go into deciding what this price should be.

The issuing company appoints investment bankers to help them decide. Investment bankers do their research about how much a company can earn in the future and what kind of cash flow it can generate, and then arrive at a valuation that is comparable to that of similar companies in the industry. This valuation then decides the price. So, say, if ABC Ltd is offering shares in an IPO at Rs.100 per share, then you know that this price takes into account how well the company can generate cash and profit in future.

Price is said to be at fair value if it has accounted for the company’s current earnings and financial health while also keeping in mind the immediate future growth. It is overvalued if the price considers growth at a higher rate than achievable. If the case is opposite—growth rate is underestimated—price is said to be undervalued.

The charm of IPOs used to be in listing gains. For IPOs that came at prices that were fair to undervalued, there was room for gains when the shares listed on exchanges. If this is not the case, there isn’t a compelling reason to choose an unlisted stock over a listed entity with a similar profile in the same industry.

Surya Bhatia, certified financial planner and managing partner, Asset Managers, said, “The days of 30-40% gains on listing on IPOs are gone. Investors have to be careful about valuations; an issue by a company with sound fundamentals but which comes at a high price may not be worth it.”

These days IPO pricing has become quite aggressive. Parag Parikh, chairman, PPFAS Asset Management Pvt. Ltd, said, “The novelty of IPOs is not there anymore; IPOs are now priced at market rates. The investment bankers want to get the maximum benefit for the company by pricing the issue at the highest possible point. This leaves nothing on the table for investors.”

Earlier as well, there were only a handful of issues where the management was cognizant about pricing so that investors make money, added Parikh.

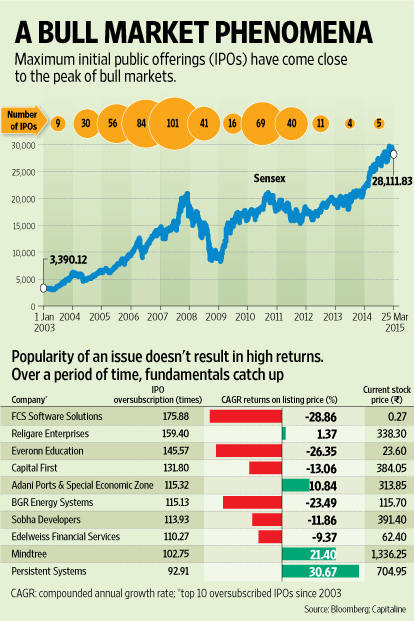

Most IPOs anyway come during bull markets, which is an excuse for the high pricing of the issue. If markets continue to move up and business fundamentals keep pace, the share price will do well. If not, eventually the market price of the share will get rationalized in line with business fundamentals.

“Companies don’t want to sell their shares in a bear market because they won’t be able to get a good price. But then where is the logic for investors to buy these shares in a bull market, when valuation is high?” said Parikh.

To be fair, there have been some good issues in the past. While companies such as Maruti Suzuki Ltd, Tata Consultancy Services Ltd, Bharti Airtel Ltd, Yes Bank Ltd and IDFC Ltd, to name just a few, have built wealth for investors over a long period of time, their IPOs too went well. Maruti Suzuki Ltd’s IPO was oversubscribed around nine times and the opening price on listing was at least 26% higher than the offer price. Similarly, Yes Bank’s issue was oversubscribed around 29 times and the stock listed at a premium of nearly 45%.

“Valuation is the key to arriving at a decision to invest in an IPO. Investors need to look at aspects such as earnings multiple, compare with peers in the industry and see if that is indeed the best option available,” said Vinay Agrawal, chief executive officer, Angel Broking Ltd.

Looking beyond

An IPO can look inviting if the business you are buying shares into is in a niche industry or a new industry. It’s an opportunity to own a piece of a business in an industry that isn’t available otherwise.

This is why seemingly there was a rush from investors across the world to apply for Facebook Inc.’s IPO, which listed in the US in 2012. As a result of the increased demand, the management not only increased the number of shares available but also bumped up the issue price.

However, as experts have repeatedly pointed out, pricing is everything. Facebook’s shares listed flat, and for days after, lost value. The shares have eventually gained thanks to newer initiatives by the company that kept growth intact.

Keep in mind that once a stock is listed, you will always be able to buy in the secondary market. If the IPO price is too high, there is a good chance of getting a better price post listing.

So, while it’s great to buy shares in a new and exciting company, you can do that even after it lists.

The Facebook example also shows that the extent of oversubscription and the size of an issue has little bearing on potential gains from your investment in the short and long run. The same holds true whether the IPO is in India, the US or elsewhere.

If you look at the domestic IPOs in the past 10 years, of the top 10 oversubscribed issues, only three have given compounded annual growth rate returns of more than 10% till date.

Besides, the more oversubscribed the issue, the lesser the allocation that you will get. Applying for shares worth Rs.2 lakh and getting an allocation worth Rs.50,000 or Rs.1 lakh may not be worth it.

If pricing is favourable, quality of management is what you want to be sure of next.

Pointing out the need to consider qualitative aspects, Agrawal said, “It’s important to also consider how the company will use the IPO funds; will the additional funding help the company generate strong revenue going forward? Be careful in instances where the funds raised are primarily going to be used for objectives such as reducing debt.”

These details reflect on the management and its ability to utilize resources efficiently.

There are alternatives

A well-priced IPO from a fundamentally sound company can be a good investment opportunity. But identifying this at the IPO stage itself is easier said than done, especially if you have to undertake research around pricing and business fundamentals.

An IPO is only your first chance to invest in a company, not your last. You can always buy in the secondary market at a later date. Or, if you are a mutual fund investor, you might get exposure to such issues through your diversified equity funds.

Mutual fund managers are better placed to identify IPO opportunities, and judge whether they are priced well and if the quality of management is good. Whenever such opportunities come up, mutual fund schemes do invest, and if you want a piece of the action, you are better off investing in mutual funds with good track records.

It’s fair to say that there is very little advantage that an IPO can offer you if it’s not priced attractively. And even if it is priced well, but the issue is oversubscribed, you may not get a good allocation in the end.

A fundamentally sound company will continue to deliver returns long after listing gains have been forgotten. Hence, in most cases it’s best to leave IPO investing to those who are well versed with how to value the initial offer price of a company.

The original article could be seen here.